A few investment norms we have been accustomed to for a long time are falling or getting disproved. What does it signify?

Gold attracts increased investor interest during high or rising inflation periods because gold is considered a good hedge against inflation; consequently, gold prices rise during such periods.

Bond yields and Stock prices have an inverse relationship: as bond yields rise, stock prices decline, and vice versa.

Gold prices and Interest rates have an inverse relationship because as interest rates rise, the opportunity cost of holding gold increases, making gold less attractive as an investment.

During an economic slowdown, central banks and governments stimulate the economy through various supportive measures, such as interest rate cuts, bond purchases, tax cuts, cash payouts, and deficit spending.

We have been accustomed to these investment norms for the last few decades. Given this, this year’s 30 per cent gain in gold prices is confounding because inflation and interest rates were either steady or declined. However, apart from being considered a hedge against inflation, investors favour gold for its reputation as a safe asset, by flocking to gold during periods of increased economic uncertainty. This year’s sharp increase in gold prices despite subdued and steady inflation likely suggests an impending period characterised by increased economic difficulties.

During economic difficulties, central banks usually inject liquidity (basically, money printing) into the financial system to safeguard and stimulate the economy. Such money-printing exercises also favour gold prices. Suppose this year’s gold price gain forecasts impending economic difficulties. In that case, bond yields should be declining, because central banks usually respond to economic slowdowns by lowering interest rates. However, contrary to expectations, bond yields have risen instead of declining despite the US Central Bank reducing interest rates twice in the past three months.

The rising bond yields likely suggest higher interest rates next year against the current consensus of lower rates. However, central banks are cutting rates now as they consider the current level of interest rates too high and restrictive. What would then cause interest rates to go up next year?

A plausible reason for the Fed to reverse its course from rate cut to rate hike next year is the reemergence of inflation as a major threat to US economic prospects. As we assumed earlier, gold prices might not be forecasting impending economic difficulties; rather, they might be forecasting higher inflation next year. But since the Fed is cutting rates now because the current level of interest rates is restrictive, would hiking rates make them even more restrictive? Yes, it would.

A possible scenario for next year is that inflation reemerges as a major threat and the Fed pivots and starts hiking interest rates to fight inflation, adversely affecting the economy. Despite the adverse economic effects, the Fed prioritises inflation taming over economic growth, exacerbating the difficulties. This would lead to a combination of low economic growth and high inflation (stagflation): a disturbing economic scenario. The developed world had its last serious case of stagflation in the 1970s, significantly damaging their economies and markets.

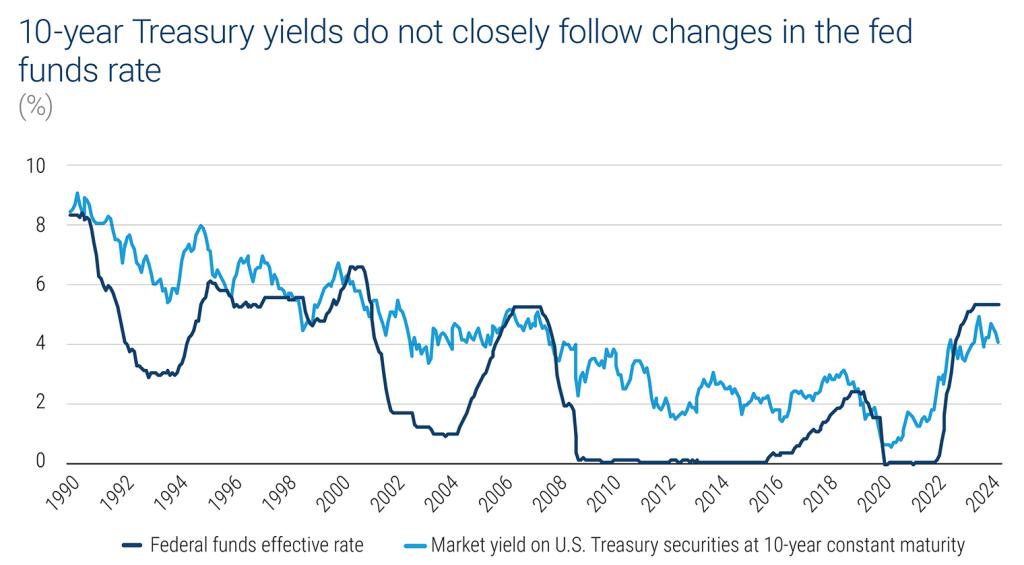

Another confounding event is the rise in 10-year US treasury yields from 3.60 to 4.22 per cent in three months since the Fed cut its policy interest rate in September 2024. It contradicts the investment norm of the positive correlation between US bond yields and Fed fund rates. The chart below illustrates the correlation between 10-year US treasury yields and Fed fund rates.

The chart shows three occasions when Fed fund rates were higher than 10-year yields over the past three decades. Although they prevailed only shortly, the occasions coincided with the major economic crises of those times. The phenomenon occurred in early 2000, coinciding with the dot-com bubble burst and the subsequent severe recession. It happened again in 2006-2007, leading up to the global financial crisis. Now, we are experiencing the third occurrence of the phenomenon over the past twenty-five years.

Normally, capital flows towards emerging markets such as India as the Fed cuts interest rates. But this investment norm too was discredited over the last three months as Indian markets witnessed one of the largest capital withdrawals by foreign investors after the Fed’s September 2024 rate cut. Consequently, the Nifty50 index is 10 per cent down from its September 2024 highs.

Indian economy won’t be insulated from the inflation risk if there is an inflation spike in the US and other developed countries because central banks in developed countries will raise interest rates to fight inflation, triggering capital flow towards the dollar. Consequently, the dollar strengthens, making our imports costlier, translating into higher prices in the domestic market. RBI will be forced to raise interest rates to counter the imported inflation and the capital outflow triggered by the strengthening dollar.

So far, no inflation spike is conspicuous in developed countries. The above discussion on the inflation spike emerged from my subjective interpretation of the rising US bond yields over the past three months.

US stock prices, which have risen 12 per cent since the September 2024 rate cut, indicate more monetary easing and better economic conditions next year, in sharp contrast to those suggested by bond yields and gold prices. Another possible economic scenario for next year is that we may have higher rates and better economic conditions.

In its November 2024 FOMC statement, the Federal Reserve said that recent indicators suggest a buoyant US economy. Inflation might spike if this buoyancy escalates into overheating. The Fed would counter this through calibrated interest rate hikes to sustain strong economic activity. Timely interest rate adjustments could help sustain robust economic activity by avoiding overheating and at the same time not being too restrictive. This scenario could explain the rising stock prices and rising bond yields. But where do the rising gold prices fit in this scenario?

The four factors of economic growth, risk and uncertainty, opportunity cost, and momentum influence gold prices. All four factors have been favourable to gold prices for some time and could plausibly explain the large gain in gold prices over the past year. Interest rate cuts were anticipated for more than a year and were cut beginning September 2024. This has reduced the opportunity cost for holding gold. Moreover, Gold prices have momentum as they have risen for the past five years. Strong economic growth and elevated risk and uncertainty have existed in the world economy for some time.

Global economic growth has been strong for the past two to three years and is expected to remain steady this and next year, as per IMF’s Oct 2024 World Economic Outlook: it projects world output growth of 3.2 per cent in 2024 and 2025. But the IMF also warns that there is high uncertainty surrounding the outlook due to probable significant shifts in trade and fiscal policy by newly elected governments, return of financial market volatility triggered by hidden vulnerabilities, heightened anxiety over appropriate monetary stance if inflation spikes or economic slowdown emerges, and further intensification of geopolitical rifts.

The inverse relationship between stock prices and bond yields was too disproved over the last three months when US stock prices increased by 12 per cent and bond yields increased by 62 basis points. There is more than one explanation for the market’s discordance with some long-held investment norms. Occasionally, market prices, particularly bond prices (or yields), have demonstrated their predictive capability by moving before an oncoming significant market event. Therefore, recent market developments could either be the failure of a few long-held investment norms or a display of the market’s predictive capability.

Subscribe

Enter your email below to receive our latest content in your Inbox.